Members Voluntary Liquidation (MVL)

A members' voluntary liquidation otherwise known as an MVL, is a procedure only available to a solvent company which enables the directors and shareholders to close down a company. A liquidator is appointed to take care of the MVL process by realising the remaining assets and discharging any remaining liabilities. The remaining funds can then be distributed to the shareholders accordingly and the company is then dissolved.

- Distributions to shareholders are required following cessation of the business (these can be done in a tax efficient manner).

- A company has ceased its operations and there are assets to be distributed.

- The shareholders are in disagreement as to the future management of the company.

- It is felt the company may start to incur losses, but is currently solvent.

- There is a need for re-organisation or reconstruction.

- The purpose for which a company was set up has been achieved.

If you are a creditor of a business that is subject to an MVL please read the creditors guide to Members Voluntary Liquidation

How does an MVL work

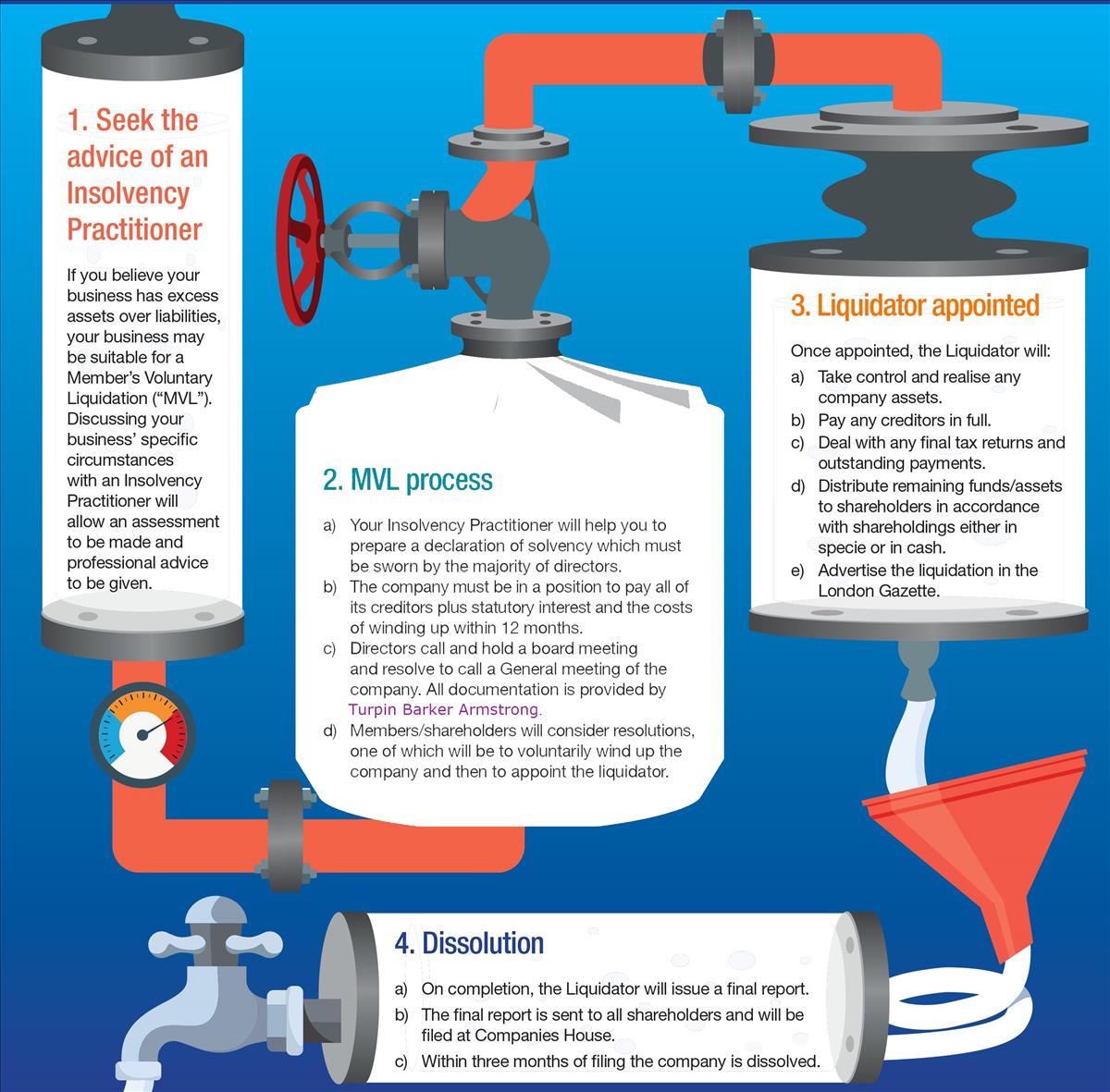

Once a director has decide to go down the MVL route they must swear a Statutory Declaration of Solvency confirming that the company has sufficient assets to discharge all its liabilities. In other words have enough funds in the company to ensure all debts are paid in full.

The shareholders must then pass a special resolution approving the liquidation and an ordinary resolution appointing a liquidator to handle the administration of the liquidation. This sounds more complicated than it is and we at turpin barker armstrong can be appointed as liquidator to assist you with the mvl process. The appointed mvl liquidator will then realise any remaining assets, discharge any remaining liabilities, and make distributions to the shareholders.

Where physical assets exist, the liquidator can distribute these "in specie" which eliminates the need for the assets to be sold. If this is necessary, the liquidator will require an independent valuation of the assets proposed to be distributed in this manner.

The key advantages of a Members Voluntary Liquidation - mvl:

- The liquidator has the ability to return funds to Shareholders as capital – which can have considerable tax advantages as all distributions will be capital repayments and subject to Capital Gain Tax (“CGT”) rules rather than PAYE/NI procedures or dividends. Directors who have been a director and shareholder of a company for at least 12 months and the company traded in that period can claim Business Asset Disposal Relief (formerly known as Entrepreneurs’ Relief) which, when coupled with the personal allowance for CGT of £11,100 with taxation currently at 10%, can be extremely favourable when compared to higher rates of PAYE.

- The liquidator has the ability to restructure a business, perhaps using a hive down and to distribute assets (or shares in subsidiaries) in specie.

- An MVL can be used as a means of resolving a shareholder dispute as the company will no longer trade, plus when the liquidation is complete the company simply ceases to exist.

- An MVL is quick and fairly cheap compared to other restructuring procedures.

We always offer the first meeting free with no obligations to commit